Microsoft Reshuffles Financial Reporting Structure

- Paul Thurrott

- Aug 22, 2024

-

0

Microsoft revealed in a regulatory filing that it will soon move numerous business segments into different top-level business units, while retaining the same three top-level businesses units as before.

The firm is touting this change as being more transparent for investors because it more closely aligns with how the business is run. But it was likely made to mask poor performance or slowing growth in key businesses at a time when the software giant is investing tens of billions of dollars per quarter building out its AI infrastructure. Microsoft’s vast growth in wealth and worth under Satya Nadella was funded in large part by Wall Street excitement about Azure and Microsoft’s future as a cloud giant. But as that business has matured, its successor, AI, has so contributed more costs than profits. By spreading those costs around, the company can more easily hide this softness.

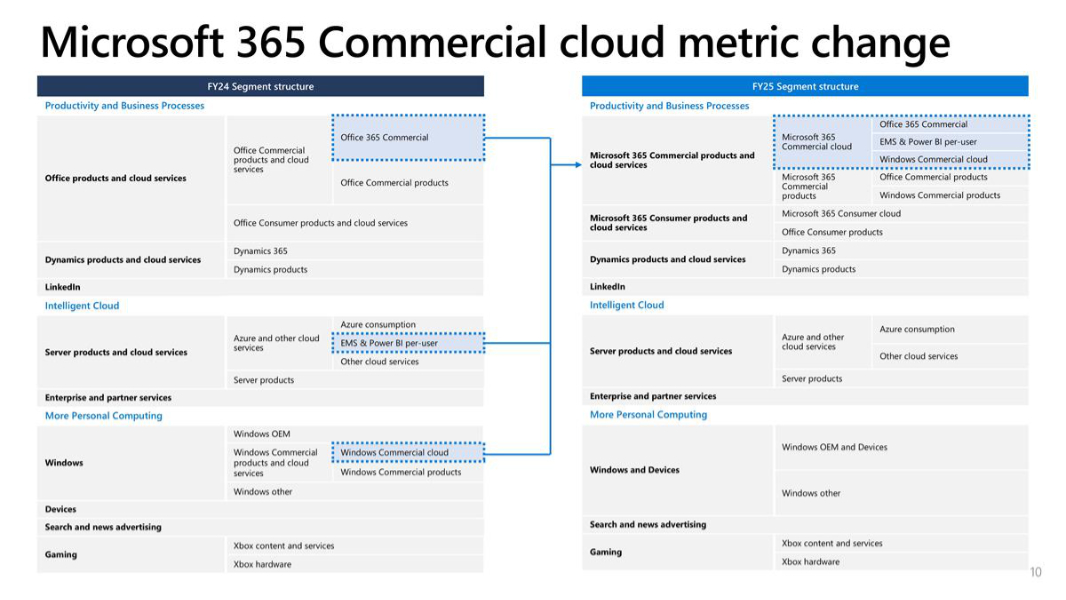

Microsoft has three top-level business units–Intelligent Cloud, Productivity and Business Processes, and More Personal Computing–and while that structure is not changing, the firm is moving numerous business segments–sub-businesses found within a top-level business unit–to other parts of the company for the purposes of financial reporting. Microsoft details these changes in a presentation that accompanies the filing.

At a high-level, it appears that Microsoft’s biggest business unit by revenue, Intelligent Cloud, is not changing: Revenues from Azure and other cloud services, Server products, and Enterprise and partner services will still fall under this unit. But there are changes. Enterprise Mobility + Security (EMS) is moving into Productivity and Business Processes (under Microsoft 365 Commercial cloud; see below). Nuance Enterprise revenue is moving from Server products to Dynamics (under Productivity and Business Processes), though Nuance Healthcare revenues will remain.

And the other two business units are changing even more.

Productivity and Business Processes has long accounted for Office products and cloud services, Dynamics products and cloud services, and LinkedIn. But for fiscal 2025, which began July 1–the current fiscal year, in other words–Office products and cloud services is being replaced by separate Microsoft 365 Commercial products and cloud services and Microsoft 365 Consumer products and cloud services business segments. And each is being split into separate cloud and products sub-segments to differentiate between subscription and perpetual licenses revenues. (Dynamics and LinkedIn are unchanged.)

To date, More Personal Computing has included Windows, Devices, Search and news advertising, and Gaming business segments. The latter two segments are unchanged. But under the new structure, Windows and Devices are merging into a single business segment. And while there will still be Windows OEM (now called Windows OEM and Devices) and Windows other sub-segments under that, the Windows Commercial products and cloud services sub-segment is gone, and is now part of Microsoft 365 Commercial cloud (under Productivity and Business Processes). So this business unit’s revenues will be significantly lower year-over-year (YOY) moving forward.

Copilot Pro revenues, previously reported under Office Consumer products and cloud services (in Productivity and Business Processes) is moving to Search and news advertising (in More Personal Computing), which could help to mitigate the lost Windows Commercial products and cloud services revenue a bit.

Microsoft says it made these changes to align its financial reporting to how the business is managed. For example, the merging of Windows and Devices will “bring revenue from PC market-driven revenue together.” It will also help mask how poorly Devices–i.e. Surface–performs, of course. Which, again, I think is the real point of these changes or, at the very least, a happy side-effect: Because of this change, Microsoft is legally required to restate revenues from last year as if they had been reported under the new structure. And when you make that change, Windows and Devices falls on its face, with 5 and 1 percent revenue shortfalls in two of the previous four quarters, and low 2 and 4 percent growth in the other two.

The next few quarters were always going to be interesting. But this change will make them even more interesting. And for people like me who obsess over these details while getting less and less information each year, it should be more confusing than ever.